UK Regulation And Responsible UFC Betting: What Every Bettor Should Know

Table of Contents

- The Rules Of The Pitch For UK UFC Bettors

- What The UKGC Actually Regulates And Why It Matters

- Age, Identity, And The Documents A UK Book Will Ask For

- Affordability Checks And Setting Limits That Work

- GamStop And Self-Exclusion: How The Hard Brake Works

- Knowing When The Hobby Has Become Something Else

- Why Offshore Books Look Cheaper Until They Don’t

- Integrity, IBIA, And Why That Refund Email Sometimes Lands

- Where To Go When You Need Help

The Rules Of The Pitch For UK UFC Bettors

There is a stretch of every fight week where I get the same question from people I know who bet UFC casually. It always sounds like a version of “is it legal”, or “are these limits real”, or “what actually happens if I lose more than I planned”. The answers depend on a regulatory framework that ufc betting uk regulation guides routinely treat as background. It is not background. It is the actual ground rules of the game, and if you don’t understand them, you’re betting blind on the only dimension of UFC wagering that the bookmaker cannot bend in your favour.

This article is the working ruleset for any British bettor who places money on UFC fights through a licensed UK operator. The UK Gambling Commission is the regulator. It oversees a market of £16.8 billion in annual gross gambling yield as of the year to March 2025, with online accounting for £7.8 billion of that and growing. The framework that sits behind those numbers — licensing, age verification, affordability checks, deposit limits, self-exclusion, integrity monitoring — is what protects you when something goes wrong, and what defines what an operator is allowed to do to you when nothing has gone wrong.

Nine years inside the industry has taught me that the regulatory layer is dramatically misunderstood by casual bettors. Most don’t know what affordability checks are until they get one. Most don’t know how GamStop works until they need it. Most don’t know what makes an integrity refund land in their email. This article walks through the framework section by section — what the UKGC actually regulates, the age and KYC walk, affordability and limits, GamStop and self-exclusion, the signals that the hobby has become something else, the offshore temptation, the integrity layer, and the support resources that exist precisely because the framework anticipates that some bettors will need them. The tone is practical. No moralising, no warnings dressed as advice. Just the rules, written by someone who has had to follow them professionally and personally.

What The UKGC Actually Regulates And Why It Matters

I once watched a senior compliance officer at a UK operator describe the Gambling Commission as “the silent referee in every transaction”. The phrase stuck because it captures the role precisely. The UKGC does not decide which fights you bet on or how. It decides the structural rules every UK operator must follow before you ever land on their site — licensing, anti-money-laundering compliance, age verification, marketing standards, technical security, segregated customer funds, dispute resolution, and the responsible-gambling tooling that has to be visible on every account.

Andrew Rhodes, the chief executive of the UK Gambling Commission, told the Betting and Gaming Council AGM in February 2025 that total gross gambling yield had reached its highest-ever level at £15.6 billion, with participation stable at 48% — just under half of the adult population in Great Britain placing some kind of bet. That figure continued to climb in the annual statistics released later in the year, settling at £16.8 billion for the period ending March 2025, a 7.3% year-on-year increase. The size of the market is the reason the regulatory framework exists in the form it does. Half the country gambles in some form. The Commission’s job is to keep the structure standing.

The licence itself is the foundation. Every UK-targeted operator must hold one. The licence number sits in the footer of the operator’s site and on the public UKGC register, and verifying it should be the first thing you do before depositing. The licence imposes binding obligations on the operator: age verification before the first deposit, anti-money-laundering checks proportional to the deposit pattern, a clear complaints route, and adherence to the technical standards that govern how the games and markets must function. None of these obligations exist on an unlicensed offshore operator.

The physical-retail layer of the UK gambling industry is shrinking but still substantial. There were 5,825 betting shops in Britain at the end of March 2025 — the 11th consecutive year of decline at roughly 1.8% annual contraction. The number of licensed gambling premises overall stood at 8,148 by the end of Q4 2025, including 191,325 gaming machines. The retail estate matters here because most of the regulatory framework was originally designed around physical shops, then translated into the online environment. The 18-plus rule, the responsible-gambling signage, the right to self-exclude — all of these originated in the shop and now live on every UKGC-licensed website.

What the UKGC does not regulate is the bookmaker’s pricing decisions. They can price a fight at whatever overround they choose, refuse to take a bet, close your account on notice (with the funds returned), or restrict your stakes. These are commercial decisions, not regulatory ones. The regulator’s role stops at the conduct boundary; the operator’s pricing strategy is theirs to set.

Age, Identity, And The Documents A UK Book Will Ask For

The minimum legal age to place any bet in the UK is 18. There are no exceptions, no carve-outs, no jurisdictional variations within the United Kingdom. The Gambling Act sets it, the UKGC enforces it, and the operators verify it on every new account through a combination of electronic identity checks against the credit agencies and document upload when the electronic check fails or returns ambiguous results.

The first verification you experience as a new UK bettor happens at the sign-up screen. The operator collects your name, date of birth, address, and contact details, then runs an electronic check against the credit reference agencies. If the check returns a confident match, your account is open and you can deposit immediately. If it does not — common reasons include a recent house move, a thin credit file, or a name spelt slightly differently than the agency holds — the operator asks for documentary verification before processing your first deposit.

The documents you’ll typically need are proof of identity (a passport or full UK driving licence) and proof of address (a recent utility bill, bank statement, or council tax letter dated within the last three months). The operator’s compliance team reviews the documents within 24 to 48 hours at most well-run UK books, though the actual turnaround varies. Some operators clear documents within an hour; others can take three days. Document-upload friction is a real part of the new-account experience and one of the legitimate reasons to compare operators on user experience before committing.

The second verification stage — source-of-funds — kicks in once your deposit pattern crosses certain thresholds. The trigger thresholds are operator-specific, but typical patterns: depositing more than £2,000 to £5,000 in a 30-day window, large single deposits, or unusual patterns relative to the demographic profile. The operator then asks for documentation showing where the money came from — bank statements, payslips, P60s, or business documents. This is anti-money-laundering work, mandated by the Proceeds of Crime Act and supervised by both the UKGC and HM Treasury. It is not optional and it is not negotiable. The operator that fails to do it loses its licence; the bettor that refuses to provide it has the account frozen or closed.

The KYC walk irritates a lot of casual bettors who feel surveilled. The honest reframing is that you’re being verified once, by a regulated operator, so that you can be confident the bettor on the other side of every transaction is also being verified, and that the operator itself is being checked by the regulator. The friction is the price of the consumer protections that come with it.

Affordability Checks And Setting Limits That Work

Affordability checks are the most discussed and least understood part of UK gambling regulation. The framework is straightforward in principle: an operator must take steps to assess whether a bettor’s gambling is financially harming them, and intervene before the harm becomes serious. The implementation has been bumpy. Andrew Rhodes addressed the communication issue at the February 2025 BGC AGM, saying the regulator and industry had to tighten their messaging because the inconsistency was unhelpful — and noting that “there are a whole host of other things going on this year” that demanded attention beyond affordability alone.

The structure of affordability checks operates on a tiered basis. The lightest tier is a passive financial-vulnerability check using credit-agency data, typically triggered by net deposits crossing the £125 mark over 30 days or £500 within 365 days under the framework being phased in. Most bettors will never see anything visible from this tier — the operator runs the check in the background and only acts if the data shows distress signals. The next tier is an active affordability assessment, triggered at higher thresholds (typically around £1,000 net loss in 30 days, though operator-specific), where the operator may ask for documentation showing the bettor can sustain the loss without financial harm. The highest tier is enhanced due diligence, kicking in for VIP-segment activity or unusual patterns, where source-of-funds and source-of-wealth documentation is required before further deposits are accepted.

The casual misunderstanding of affordability checks is that they are punishment for losing money. They are not. They are a safety net designed to identify gambling that is causing financial harm and slow it down before the harm compounds. From the bettor’s perspective, the practical advice is to be prepared for the documentation request when your deposit pattern crosses operator thresholds, and to use the responsible-gambling tools proactively so that the checks find a sustainably-bounded account rather than an out-of-control one.

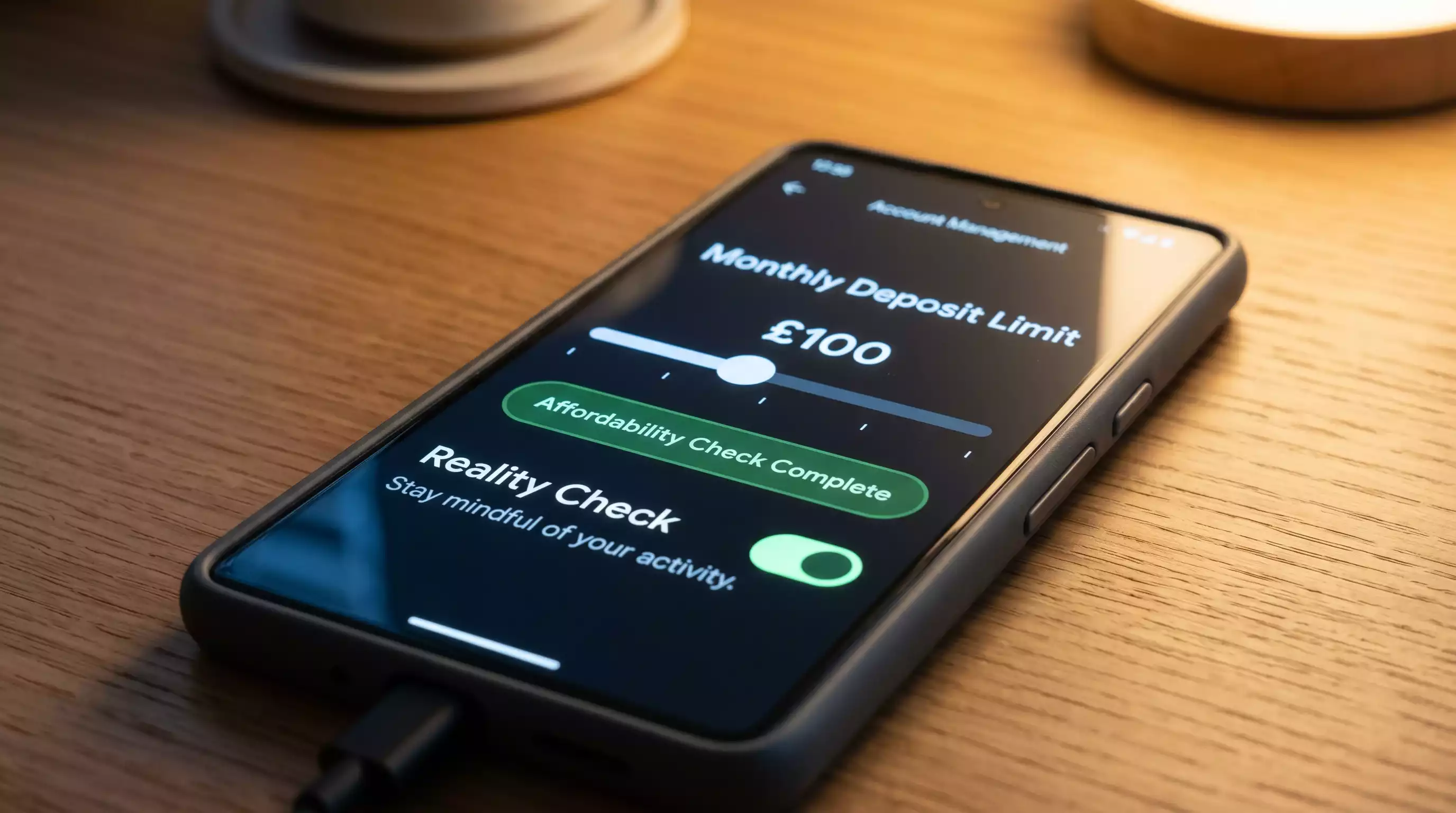

Deposit limits are the single most useful tool any UKGC-licensed account offers. You set a per-day, per-week, or per-month cap on what you can fund the account with. The cap is enforceable in real time — the operator’s system blocks the deposit once you hit the limit, no exceptions. Setting the limit takes 30 seconds. Removing it takes longer, because the UKGC requires a 24-hour cool-off period on any limit increase to prevent emotional decisions from undoing your own brakes.

The honest tactical advice on deposit limits is to set them at a level that is genuinely sustainable for your finances, not at a level that “feels reasonable” in a high-anticipation moment before a fight night. The figure you’d be comfortable losing entirely, with no impact on rent, bills, or savings, is the upper bound. Most bettors set it too high because they think of the limit as a ceiling for big nights rather than a floor for normal weeks. The number that feels too cautious is usually closer to the right number.

Loss limits work similarly to deposit limits but track net loss rather than gross deposit. They are slightly stricter as a brake because they account for winnings being re-staked. Session time-outs interrupt your play after a defined period and require you to actively log back in. Reality checks pop up at intervals to show you how long you’ve been playing and how much you’ve staked. All of these are required on every UKGC account; whether you use them is your choice, and you should.

GamStop And Self-Exclusion: How The Hard Brake Works

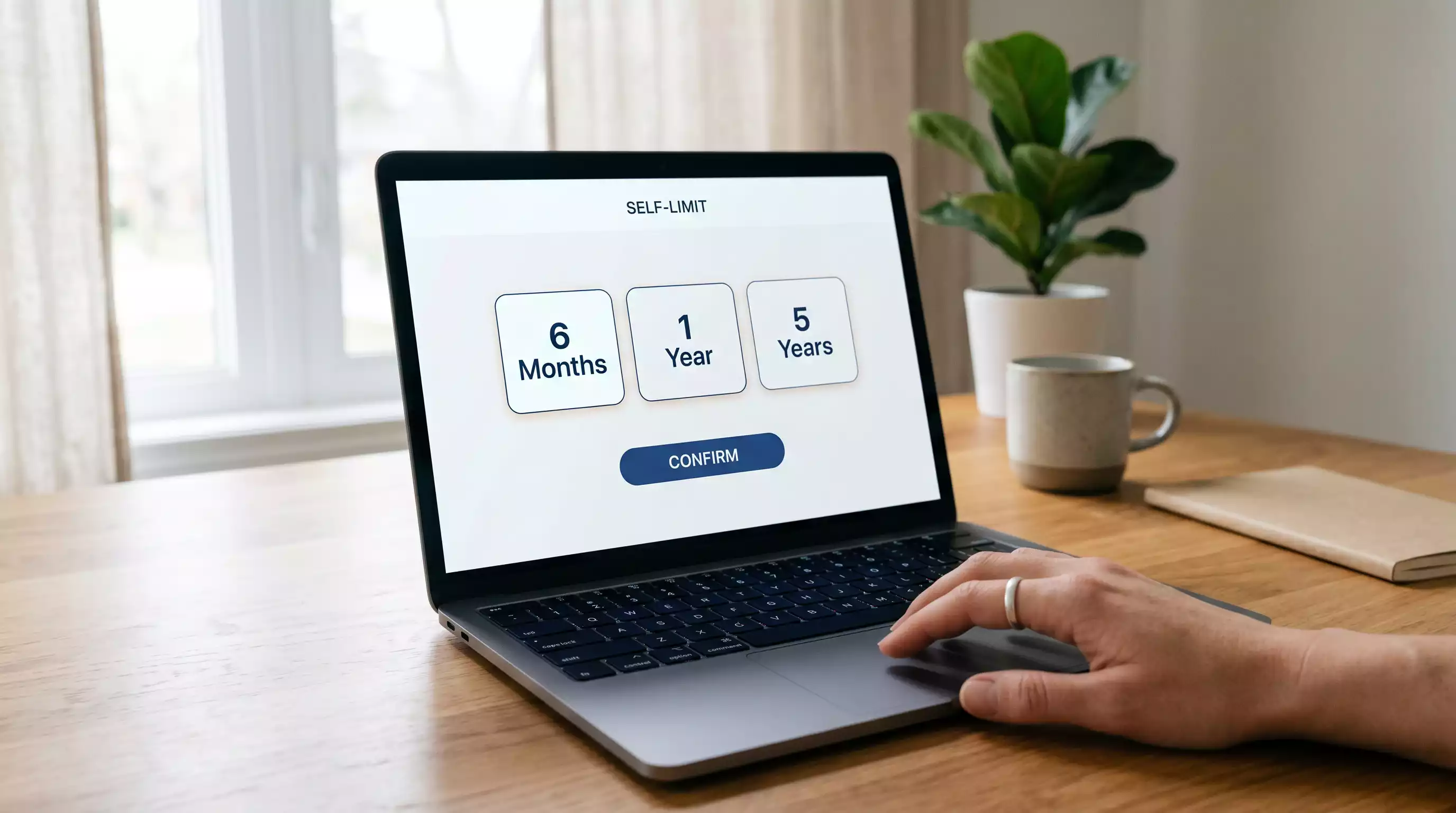

GamStop is the national self-exclusion service for UK online gambling. Every UKGC-licensed operator participates — it is a condition of the licence. When you register with GamStop, you choose an exclusion period of 6 months, 1 year, or 5 years, and during that period every UKGC-licensed operator is required to block your sign-ups and refuse your deposits. The block applies across the whole licensed sector, not just the operator you originally had a problem with.

The mechanism is straightforward. You go to the GamStop website, register with your personal details, choose the exclusion period, and the system propagates your details to the participating operators within 24 hours. From the moment of registration, you cannot open a new account or deposit into an existing one at any UKGC-licensed site. Existing balances can usually be withdrawn during the exclusion, but new bets cannot be placed.

The exclusion period is not pause-able. Once you’ve started it, you cannot end it early. This is by design. The point of a hard brake is that it cannot be released in the moments when releasing it would be most damaging. If you change your mind a week into a 12-month exclusion, the answer is no — you wait the full 12 months, and the regulatory structure exists precisely so that no operator can offer you a way around it.

The structural reason GamStop matters is that the UKGC perimeter is the only place this brake works. Offshore operators are not bound by GamStop. If you exclude through GamStop and then look for a non-UK-licensed site to bet at, the exclusion is meaningless against that site — and the consumer protections you’d lose by going there compound the original problem you were trying to solve. GamStop is therefore only as effective as your discipline to stay inside the licensed UK perimeter during the exclusion period.

There is also a single-operator self-exclusion route, separate from GamStop, where you ask one specific operator to close your account for a defined period. This is useful if you’ve had a problem with a particular site but want to retain the option to bet elsewhere. The structural caveat is that it does not propagate; it binds only the operator you’ve requested it from. For most bettors who need the brake, GamStop is the stronger tool because it removes the option to switch sites.

The first registration step takes about 10 minutes on the GamStop site, including the identity verification. The decision itself is harder than the form. The framework exists for people who need it; if you’re reading this section and recognising yourself in it, that is itself a signal worth taking seriously.

Knowing When The Hobby Has Become Something Else

The Problem Gambling Severity Index — PGSI — is the screening tool the academic community uses to assess gambling-related harm. It is a nine-question instrument that scores behaviours, feelings, and consequences over the prior year. A score of 8 or higher is categorised as problem gambling. A score of 3 to 7 is moderate-risk. A score of 1 to 2 is low-risk. The latest Gambling Survey for Great Britain estimated that 2.7% of UK adults score PGSI 8 or higher, with 3.1% in the moderate-risk band and 8.8% in the low-risk band. Among adults aged 18 to 24, the problem-gambling rate climbs to around 10% — a meaningful elevation that reflects the demographics most exposed to fast-result digital betting products including UFC.

The signals the PGSI measures are behavioural rather than financial. The questions ask about chasing losses, increasing stakes to maintain excitement, betting more than intended, feeling guilty about gambling, feeling that gambling has caused stress or anxiety, betting beyond means, borrowing or selling possessions to fund gambling, and gambling causing problems in relationships or work. The score is the sum of these signals over the prior 12 months.

The pattern that’s specific to MMA and UFC betting — and that I’ve watched play out in conversations with people I know — is the parlay chase after a string of losing single bets. A bettor loses two or three moneylines on prelims, decides to “make it back” on a four-leg accumulator on the main card, loses that, and then sizes up the next bet larger to compensate. Each step looks rational in the moment; the pattern, when stepped back from, is a textbook chasing sequence. The bookmaker structure makes this pattern easy to repeat because the parlay multipliers always promise a single-bet path back to break-even.

The behavioural signal I’d ask anyone to honestly self-check on is: am I betting amounts I would have called reckless three months ago? If the answer is yes and the trajectory is upward, that is the moment to pull the deposit limit down rather than to argue with yourself about whether the current stake is “still reasonable”. The reframing is from absolute thresholds (£X is too much) to trajectory (the stake is growing in a direction I would not have endorsed in advance).

The honest framing is that gambling-related harm sits on a spectrum, and the spectrum can shift in both directions. Low-risk behaviour can compound into moderate-risk over months; equally, awareness and tooling can pull a moderate-risk pattern back toward low-risk. The framework supports both directions. The tools are there. The decision to use them is yours, and the earlier in the trajectory you use them, the lower the cost. A deeper breakdown of how the academic signals map onto UFC-specific betting patterns and the support resources that match each stage sits in a separate problem gambling support guide for UFC bettors.

Why Offshore Books Look Cheaper Until They Don’t

The offshore betting market — sites that target UK customers without holding a UKGC licence — has grown from £5 billion in 2019 to £16.6 billion in 2025. The share of UK betting activity going to licensed operators has fallen from 97% to 92% over the same period, and H2 Gambling Capital projects the offshore figure could reach £33 billion by 2028 if the regulatory framework does not adapt. That trajectory means roughly one in every five online betting pounds in the UK may be flowing offshore within three years. The structural pressure is real, and the casino around it deserves an honest look.

The visible appeal of offshore sites is the headline price. An offshore operator does not pay UK gambling duty, which means the moneyline on a UFC main might display at fractionally better odds than the UKGC-licensed equivalent. The appeal is also the absence of friction — no UKGC-mandated affordability checks, no source-of-funds requests, no deposit limits prompted at sign-up, no GamStop blocks. For a bettor who finds the regulatory friction irritating, the offshore alternative looks like the same product with less surveillance and slightly better prices.

The structural problem is that the offshore operator gives you the protections it chooses to give you, not the protections the law requires. There is no segregated-funds requirement on most offshore licences — your balance is part of the operator’s working capital. There is no independent dispute resolution; the operator’s complaints process is the operator. There is no GamStop integration — if you’ve self-excluded through GamStop, the offshore site will happily take your deposit. There is no advertising restriction, no source-of-funds review, no audit trail.

The practical consequences show up at withdrawal. The forum I’ve watched over the years is full of offshore-account horror stories: months-long withdrawal delays, demands for documentation never required at deposit, sudden account freezes citing “violations” that the operator never explained, balances that simply disappear when the operator’s licence in the host jurisdiction is revoked. None of these patterns appear at a UKGC-licensed operator because the regulatory structure makes them unprofitable to engage in. They appear at offshore operators because the operator is not bound by anything the UK regulator can enforce.

The headline-price advantage of offshore is also less than it looks once you’ve factored in the protections you’re giving up. The implicit cost of a 1% better price is the implicit insurance you’ve forfeited on the rest of the relationship. The bettors I know who’ve moved back from offshore to UKGC after a bad experience invariably describe the trade as an obvious win, not a sacrifice. The discipline is to take that lesson before learning it the expensive way.

Integrity, IBIA, And Why That Refund Email Sometimes Lands

The integrity layer of UFC betting is the least visible but most consequential structural protection in the framework. IBIA — the International Betting Integrity Association — operates a monitoring platform that tracks betting activity across more than 80 sports and 1.5 million matches per year, watching for the patterns that indicate match-fixing or insider activity. In 2025 IBIA registered 300 alerts about suspicious activity — a 29% jump from 232 in 2024.

The IBIA framework matters to MMA betting because the sport’s individual-athlete structure makes it potentially vulnerable to integrity events. A fighter is not constrained by a team result; a single bad-faith actor can in principle affect the outcome in ways that would be harder in a team sport. The framework is designed to catch the betting-side signal of those events before the integrity damage spreads.

The most concrete recent example came on 1 November 2025, when UFC terminated its contract with Isaac Dulgarian after IC360 — an integrity-monitoring service — flagged suspicious activity on his bout at UFC Vegas 110. Caesars and DraftKings, which had taken substantial action on the fight, both refunded every settled bet across the entire bout. The integrity refund is the visible consequence of the framework working: when the platform detects a pattern that warrants action, the action is taken before settled stakes are lost to a corrupted outcome.

For the UK bettor, the integrity layer manifests as the small print in the bookmaker’s terms about voided bets in the event of “integrity-related” findings, and the occasional refund email after a fight has ostensibly settled. Both of these are features, not bugs. They are the framework absorbing the cost of corrupted outcomes so that you don’t have to. The trade-off is that integrity refunds do not include payouts you’d have earned on a clean outcome — you get your stake back, not your imagined win. That is the right policy structure, even if it occasionally produces frustration.

The disciplined bettor reads the operator’s integrity policy before depositing. Look for explicit language about IBIA participation, IC360 monitoring, the conditions under which bets will be voided, and the refund mechanics. The major UK operators all have this language somewhere in their terms. The offshore sites typically don’t, and the absence of the language is itself a structural signal about how the operator handles integrity events.

Where To Go When You Need Help

The support resources for UK gambling-related harm are extensive, well-funded, and consistently rated as among the best in the world. The challenge is not their existence; it is the threshold of asking for help. Lowering that threshold is the entire job of this section. Below are the resources I’d point any UK bettor toward, organised by what they offer.

GambleAware is the UK charity that commissions independent research on gambling-related harm and funds prevention and treatment services across England, Scotland, and Wales. Their consumer-facing service is the National Gambling Helpline, reachable on 0808 8020 133, free from any UK phone, 24 hours a day, seven days a week. The helpline is staffed by trained advisors who can talk you through where you are, what options exist, and what next steps make sense. It is also anonymous if you want it to be.

GamCare runs the treatment side of the support framework. They operate the National Gambling Helpline alongside GambleAware-funded services, deliver one-to-one and group therapy through their network of treatment partners, and run online forums and chat services for bettors who prefer not to start with a phone call. The treatment is free at the point of use across the UK.

GamStop, as covered earlier, is the self-exclusion register. Register through their site directly; the process takes about 10 minutes. The exclusion is binding across every UKGC-licensed operator from the moment of registration.

Citizens Advice provides free, confidential support for the financial side of gambling-related harm — debt management, bankruptcy guidance, dealing with creditors, and accessing benefits. Their gambling-specific resources are available through the main Citizens Advice helpline and online portal.

The local NHS route depends on where you live in the UK. England has a national network of NHS gambling clinics with referral pathways through GPs and via direct self-referral on the NHS website. Scotland and Wales have similar but smaller networks. Northern Ireland’s coverage is more limited but accessible through the NHS structure.

The single most useful action any bettor reading this section can take is to put the National Gambling Helpline number — 0808 8020 133 — somewhere you can find it without having to look. The threshold for asking for help is always lower in advance than it is in the moment. The framework exists. The people on the other end of the line are skilled, kind, and not in a hurry. There is no version of this conversation where reaching out is the wrong move.

Are UK gambling losses on UFC bets taxable?

No. Gambling winnings and losses are not taxable for the UK bettor under current law. HMRC has explicitly stated that gambling is not a trade for tax purposes, so winnings are received tax-free and losses cannot be offset against other income. The bettor’s relationship with HMRC is essentially neutral on gambling activity. The tax burden sits on the operator, which pays UK gambling duty on its gross gambling yield.

How quickly does a GamStop registration take effect on a UK UFC betting account?

Within 24 hours of registration, GamStop propagates your details to every UKGC-licensed operator. Within that window, existing accounts are typically blocked from new deposits and new sign-ups are refused. The block is binding across the entire licensed UK sector for the duration of the chosen exclusion period (6 months, 1 year, or 5 years), and cannot be paused or ended early.

What is an affordability check and will I get one for UFC bets?

An affordability check is the operator’s assessment of whether your betting is financially sustainable for you. The framework is tiered: passive credit-agency checks run in the background at low deposit thresholds, active documentation requests are triggered at higher thresholds (typically around £1,000 net loss in 30 days), and enhanced due diligence applies to VIP-pattern activity. Most casual UFC bettors will never see anything visible from the lighter tiers; the active documentation request kicks in only above the threshold the operator has set.

Created by the ”bet on ufc Fight” editorial team.